How to develop a Credit Scorecard in Python

The company I work for is updating the modelling process and migrating all the scripts to Python and R. Given that a broad portion of the credit models deployed involve a binary classification, there is a need to transform variables to compute their Weight of Evidence (WOE). During my research I couldn’t find a widely-adopted framework to do the whole model from scratch, so I decided to use different tools to create one. In this post I will review some of the advantages and pitfalls I encountered during the process.

Let’s start by importing the libraries and the HMEQ dataset, that contains baseline and loan performance information for 5,960 recent home equity loans and a binary target variable.

import numpy as np

import pandas as pd

! pip install sidetable

import sidetable

import matplotlib.pyplot as plt

%matplotlib inline

import seaborn as sns

# load data

df = pd.read_csv('https://raw.githubusercontent.com/Carl-Lejerskar/HMEQ/master/hmeq.csv')

df.head()

| BAD | LOAN | MORTDUE | VALUE | REASON | JOB | YOJ | DEROG | DELINQ | CLAGE | NINQ | CLNO | DEBTINC | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 1100 | 25860.0 | 39025.0 | HomeImp | Other | 10.5 | 0.0 | 0.0 | 94.366667 | 1.0 | 9.0 | NaN |

| 1 | 1 | 1300 | 70053.0 | 68400.0 | HomeImp | Other | 7.0 | 0.0 | 2.0 | 121.833333 | 0.0 | 14.0 | NaN |

| 2 | 1 | 1500 | 13500.0 | 16700.0 | HomeImp | Other | 4.0 | 0.0 | 0.0 | 149.466667 | 1.0 | 10.0 | NaN |

| 3 | 1 | 1500 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 4 | 0 | 1700 | 97800.0 | 112000.0 | HomeImp | Office | 3.0 | 0.0 | 0.0 | 93.333333 | 0.0 | 14.0 | NaN |

As we can see from the table there are quite a few missing for several variables. To continue, let’s check the class balance of the target variable.

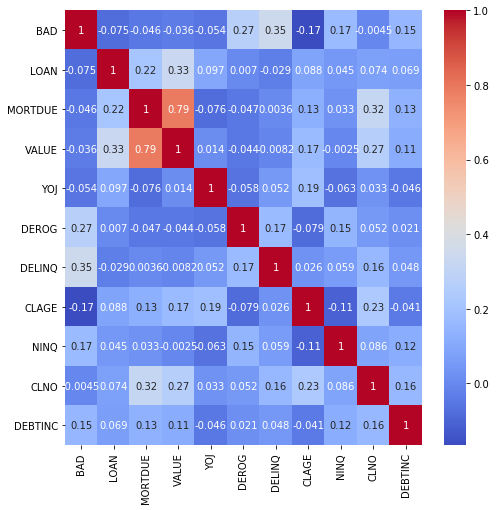

We can check correlation with the target variable using a simple Heatmap.

f, ax = plt.subplots(figsize=(8, 8))

ax = sns.heatmap(df.corr(),

cmap = 'coolwarm',

annot = True)

WOE transformation

Next we will transform our variables into WOEs. To do that, we will use 2 python libraries: scorecardpy and Monotonic WOE Binning. The reason to use both packages is that, while the former will perform the whole sequence of transformation-estimation-performance analysis, the latter will assure the monotonicity property of WOEs.

Let’s go ahead and import the libraries

#!pip install scorecardpy

#!pip install monotonic-binning

import scorecardpy as sc

from monotonic_binning.monotonic_woe_binning import Binning

Data Split and WOE computation of numeric variables

We will define a function to compute numeric variables with the monotonic_binning package.

# Perform a 70 / 30 split of data

train, test = sc.split_df(df, 'BAD', ratio = 0.7, seed = 999).values()

# Function to compute WOEs

var = train.drop(['BAD', 'REASON', 'JOB'], axis = 1).columns

y_var = train['BAD']

def woe_num(x, y):

bin_object = Binning(y, n_threshold = 50, y_threshold = 10, p_threshold = 0.35, sign=False)

global breaks

breaks = {}

for i in x:

bin_object.fit(train[[y, i]])

breaks[i] = (bin_object.bins[1:-1].tolist())

return breaks

woe_num(var, 'BAD')

This will return a dictionary that we will pass as argument to the scorecard package. But before that, we need to compute the WOEs for cathegorical variables.

# Check categorical variables names

bins = sc.woebin(train, y = 'BAD', x = ['JOB', 'REASON'], save_breaks_list = 'cat_breaks')

# import dictionary

from cat_breaks_20200724_164925 import breaks_list

breaks_list

# merge

breaks.update(breaks_list)

print(breaks)

WOE transformation

Finally it’s time to use the dictionary of WOE-rules and apply them to the original variables in train/test.

bins_adj = sc.woebin(df, 'BAD', breaks_list= breaks, positive = 'bad|0') # change positive to adjust WOE to ln(GOOD / BAD)

# converting train and test into woe values

train_woe = sc.woebin_ply(train, bins_adj)

test_woe = sc.woebin_ply(test, bins_adj)

# Merge by index

train_final = train.merge(train_woe, how = 'left', left_index=True, right_index=True)

test_final = test.merge(test_woe, how = 'left', left_index=True, right_index=True)

And now we are all set to estimate a model! Before that, some useful tips:

- Notice that we are computing WOE = ln(good/bad), by changing the

positiveparameter of thewoebinfunction. - Take into account that we need to fill the missing values if we decide to keep the original variables (as well as the transformed ones).

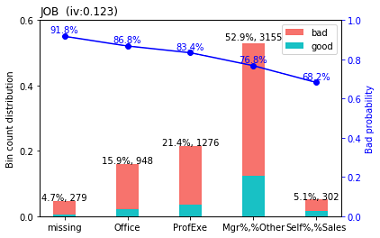

- You can manually adjust the cut-offs by calling the

woebin_adjmethod, and you can visually inspect the new variables withwoebin_plot. An example of this plot is presented below.

Logistic Regression

1. Data split and model fit

Let’s fit a Logistic Regression for the database we constructed.

# Data split

y_train = train_final.loc[:,'vd']

X_train = train_final.loc[:,train_final.columns != 'vd']

y_test = test_final.loc[:,'vd']

X_test = test_final.loc[:,train_final.columns != 'vd']

# LR fit

# logistic regression ------

from sklearn.linear_model import LogisticRegression

lr = LogisticRegression(penalty = 'l1', C= 0.9)

lr.fit(X_train, y_train)

print(lr.coef_)

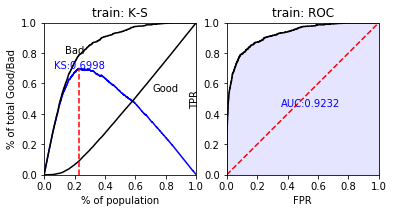

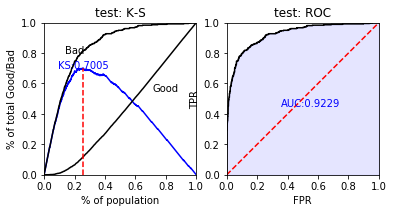

2. Performance

The scorecard package has some in-built methods to analyze performance

# predicted proability

train_pred = lr.predict_proba(X_train)[:,1]

test_pred = lr.predict_proba(X_test)[:,1]

# performance ks & roc ------

train_perf = sc.perf_eva(y_train, train_pred, title = "train")

test_perf = sc.perf_eva(y_test, test_pred, title = "test")

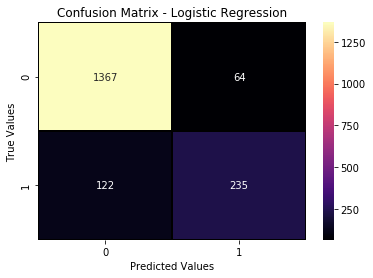

print(classification_report(y_test,predictions))

conf_log2 = confusion_matrix(y_test,predictions)

sns.heatmap(data=conf_log2, annot=True, linewidth=0.7, linecolor='k', fmt='.0f', cmap='magma')

plt.xlabel('Predicted Values')

plt.ylabel('True Values')

plt.title('Confusion Matrix - Logistic Regression');

Wrap up

This entry presented an easy way to calculate WOEs and fit a simple model for Finance and Credit analysis. I’m aware that there are many things missing from the analysis (variables selection by IV, hyperparameters tuning, among others) but I wanted to focus only on the key steps to increase performance by transforming variables to WOEs. If you have a better way to deal with these issues, or you’ve been implementing a better solution, please contact me so that I can learn from your progress.

Extras

- Jupyter notebook of the project.

- An open repo that deals with WOE transformation through a series of functions.